Net interest income

BD million

Total equity

BD million

Customer deposits

BD million

Loans and advances

BD million

Total assets

BD million

The key financial indicators of the Bank remain healthy with a return on average assets of 1.3 percent and a return on average equity of 11.4 percent.

Overview

The COVID-19 pandemic resulted in unprecedented challenges and decline in profitability across various economic sectors. As a socially responsible financial institution, our priority during such a difficult time was to support our communities and our customers to alleviate the negative impact of the crisis. In addition, preserving the Group’s liquidity and capital was a top priority, and the Group successfully achieved this as evident from its robust liquidity and capital indicators. The drop in profitability was anticipated and in line with the trend in the banking industry.

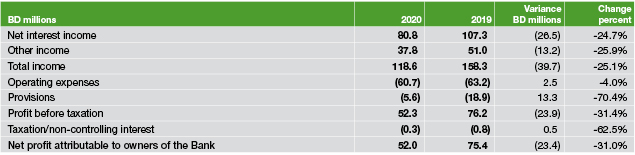

The Group managed to achieve a net profit, attributable to the owners of the Bank, of BD 52.0 million for the year ended 31 December 2020, representing a decrease by 31.0 percent over 2019 results.

The key financial indicators of the Group remain strong with a return on average assets of 1.3 percent and a return on average equity of 11.4 percent. Due to the drop in the profitability, the basic and diluted earnings per share also decreased from 56 fils to 39 fils. The Group managed to maintain a comfortable liquidity position this year, as its liquid assets to total assets reported at 34.8 percent by end of the year 2020 compared to 34.4 percent by end of the year 2019.

This section provides a review of our Group’s financial performance, focusing on the consolidated operating results and BBK’s consolidated statement of financial position, including its overseas branches, subsidiaries, joint ventures, associated companies, and indirect investment in associates through subsidiaries.

The consolidated financial statements have been prepared and are presented in accordance with the International Financial Reporting Standards as modified by CBB, and in conformity with the Bahrain Commercial Companies Law and the CBB and Financial Institutions law, and the CBB rulebook and CBB directives, regulations and associated resolutions, rules and procedures of the Bahrain Bourse and the terms of the Bank’s memorandum and articles of association.

Operating results

The net profit for 2020 decreased by 31.0 percent from last year, amounting to BD 52.0 million. The total operating income for the year decreased by 39.7 million or 25.1 percent (standing at BD 118.6 million), mainly due to the drop in net interest income and fees and commission due to the impact of the global pandemic, in addition to the decline in the Group’s share of profit or loss from associated companies and joint ventures during the year as a result of the adverse impact of the global pandemic on the financial performance of the Bank’s associated companies.

BBK’s continuous investment in boosting the management of credit risk, active management of distressed exposures and step-up in remedial efforts resulted in a significant reduction in net provision charges from BD 18.9 million during 2019 to BD 5.6 million during 2020, a decrease of 70.4 percent.

Net interest income

The steep cuts of global interest rates by central banks around the world starting from the fourth quarter of 2019 resulted in a drop in net interest income by 24.7 percent to BD 80.8 million (2019: 107.3 million).

Other income

Other operating income consists of non-interest income, derived from business activities such as dealing in foreign currencies, investing in funds other than fixed-income funds, the sale of corporate banking and retail banking services, investment trading, and income from associated companies and joint ventures.

Total other income (including share of results from associated companies and joint ventures) reported for the year 2020 stood at BD 37.8 million compared to BD 51.0 million reported for the year 2019. The net fees and commission, being the main component of total other income; stood at BD 19.6 million, compared to BD 26.6 million reported last year. The drop is mainly due to the impact of concessionary measures taken in response to the pandemic and due to the new regulations on capping fees and charges. The Bank’s share of profit from associated companies and joint ventures decreased from BD 6.8 million during 2019 to a loss of BD 0.1 million during 2020 as a result of the adverse impact of the global pandemic on the financial performance of the Bank’s associated companies and joint ventures. Other income relating to foreign exchange and investment income increased slightly from BD 17.6 million to BD 18.3 million during the year 2020.

Summary of the consolidated statement of profit or loss

Operating expenses

Despite the continuous investment in human capital resources, technologies and the implementation and achievement of many strategic initiatives, the Group’s operating expenses decreased by 4.0 percent, from BD 63.2 million to BD 60.7 million. Staff costs decreased by 7.9 percent, while non-staff related costs increased by 2.0 percent to reach BD 25.6 million (2019: BD 25.1 million). Nevertheless, the Bank’s prudent cost control policy and strong revenue-generating capability enabled it to maintain a cost to income ratio of 51.2 percent (2019: 40.0 percent).

Net provisions

The Group follows the International Financial Reporting Standard 9 (IFRS 9) with regards to accounting for the impairment of financial assets. IFRS 9 replaces the incurred loss model in IAS 39 with an expected credit loss model. The Group applies a three-stage approach to measuring expected credit losses on financial assets carried at amortised cost and debt instruments classified as FVOCI (fair value through other comprehensive income). Assets migrate through three stages based on the significant change in credit risk since initial recognition. This approach of provisioning for impairment of the Bank’s financial assets is aimed at providing more realistic estimates of the impairment in the value of assets.

The net provision charges during 2020 amounted to BD 5.6 million, compared to BD 18.9 million in 2019. The decrease was due to active management of credit risk and distressed exposures and higher recovery efforts.

Comprehensive income

The Bank’s total comprehensive income, attributable to the owners of the Bank, stood at BD 28.9 million for the year ended 31 December 2020, compared to BD 109.3 million for the year ended 31 December 2019. The drop is mainly due to the decrease in valuation of investment securities due to the impact of the pandemic on financial markets and lower net profit.

Financial position

The Group maintained its strong financial position and comfortable liquidity.

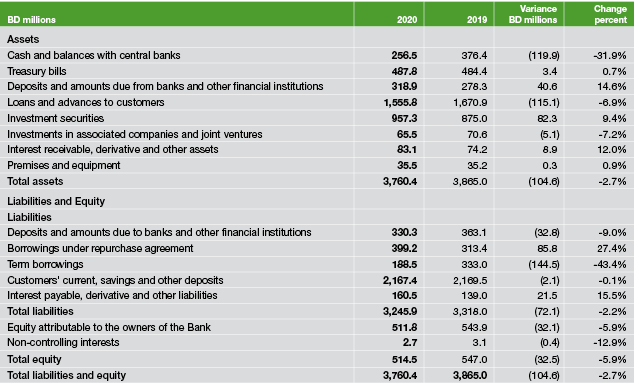

As at end of 2020, the total assets of the group stood at BD 3,760.4 million (2019: BD 3,865.0 million).

The Bank has been consistent in achieving a good balance between deposits and loans and advances with a comfortable ratio of net loans and advances to customer deposits of 71.8 percent as of end of 2020 (2019: 77.0 percent).

Assets

Total assets stood at BD 3,760.4 million as at 31 December 2020, a decrease of 2.7 percent over BD 3,865.0 million recorded in the previous year. Net loans and advances decreased by 6.9 percent to stand at BD 1,555.8 million (2019: BD 1,670.9 million), while the investment securities portfolio registered a healthy increase of 9.4 percent to stand at BD 957.3 million compared to BD 875.0 million as end of December 2019.

Liabilities

The funding structure of the Group remain strong with minimal reliance on the interbank market. Customer deposits remained the main source of funding, representing 66.8 percent of total liabilities. The Group continued to grow its retail customer base, increasing its retail liabilities to BD 1,053.3 million (2019: BD 901.4 million), while the total customer deposits maintained its levels to stand at BD 2,167.4 million as of end of December 2020 (2019: BD 2,169.5 million). Borrowing under repurchase agreements and term borrowings remain integral parts of the bank’s medium and stable funding sources, with the former standing at BD 399.2 million at the end of the year (2019: BD 313.4 million), and the latter standing at BD 188.5 million at the end of the year (2019: BD 333.0 million) as a result of repayment of USD 400 million senior debts during the first quarter of 2020.

Consolidated statement of financial position

Capital adequacy

The Bank has implemented the Basel III framework for the calculation of capital adequacy since January 2015, in accordance with Central Bank of Bahrain guidelines.

Total equity, attributable to the owners of the Bank, stood at BD 511.8 million at the end of 2020 (2019: BD 543.9 million). The decrease of 5.9 percent is mainly attributed to the negative valuation of investment securities due to market volatility and the impact of the concessionary measures taken in response to the pandemic to support Bahraini citizens and companies in addition to the dividend payments during the year. The Bank maintained its capital adequacy ratio at 21.8 percent, compared to 21.7 percent at the end of the previous year, well above CBB’s minimum regulatory requirement of 14.0 percent for Domestic Systemically Important Banks (D-SIBs). The Group is keen to maintain strong capitalisation to support future strategic plans, through adoption of dynamic profit retention policy.

Maintaining such healthy ratio is a result of our sustained culture of superior performance, our widespread participation in both local and international markets, and excellent customer service, which enables us to sustain the momentum we have built over the years and to enhance value for shareholders.